Познакомьтесь с Neo — вашим Co-GP на базе ИИ.Узнать больше

Внутренняя структура компаний по инвестициям в недвижимость: роли, должности и команды | Covercy

Операции GP·11 мин. чтения

Внутренняя структура компаний по инвестициям в недвижимость: роли, должности и команды

Как инвестиционные компании в сфере недвижимости организованы изнутри: приобретение активов и управление ими, работа с инвесторами, бэк-офис, должности, вознаграждение в зависимости от AUM и технологический стек.

Doron Cohen··11 мин. чтения

«Компания в сфере недвижимости» — понятие широкое. Это может быть жилищный брокераж с пятьюдесятью агентами, национальный девелопер, публично торгуемый REIT или спонсор из четырёх человек, управляющий единственным value-add фондом из коворкинга. Их организационные структуры совершенно не похожи друг на друга. Эта статья посвящена частному сегменту рынка: private equity-спонсорам, синдикаторам и управляющим фондами, которые привлекают капитал от аккредитованных инвесторов и институциональных LP. Именно в таких компаниях организационная структура напрямую определяет, как капитал привлекается, инвестируется и возвращается.

Органиграмму любой инвестиционной компании удобно читать, задавая себе вопрос: что должен делать этот бизнес? Спонсор обязан находить сделки, проводить их андеррайтинг, выигрывать их, финансировать, управлять активами после закрытия, привлекать капитал для всего вышеперечисленного и отчитываться перед инвесторами и налоговыми органами за каждый доллар. Штат формируется под эти задачи. Чем меньше компания, тем больше таких задач приходится на одного человека. По мере роста каждая из них превращается в отдельное направление, затем в команду, затем в департамент с руководителем, подотчётным топ-менеджменту.

Два трека, определяющих фронт-офис

В подавляющем большинстве инвестиционных компаний в сфере недвижимости фронт-офис делится на два трека: приобретение активов (acquisitions) и управление активами (asset management). Это принципиально разные функции с разным складом характера, и специалисты, как правило, строят карьеру внутри одного из них.

Acquisitions — это сторона поиска и заключения сделок. Аналитики и ассоциаты этого трека строят модели андеррайтинга, проводят исследования рынка и готовят инвестиционные меморандумы для одобрения сделки. Они живут в Excel и ARGUS. Старшие специалисты по acquisitions большую часть времени уделяют отношениям: работают с брокерами, выезжают на рынки, ведут переговоры с продавцами и партнёрами по капиталу, выбирают достойные сделки. Поиск — это контактный вид спорта, и те, кто в нём преуспевает, годами формировали брокерскую сеть, которая обеспечивает им внебиржевые предложения.

Asset management начинается там, где заканчивается acquisitions. После закрытия сделки управляющий активом отвечает за его результат вплоть до выхода — а это может занять пять-семь лет. Это означает работу со сторонним управляющим недвижимостью, контроль бизнес-плана относительно модели, рефинансирование и капитальные проекты, а также подготовку актива к продаже. Управляющие активами взаимодействуют с подрядчиками и поставщиками, ведут финансовый анализ на уровне объекта и несут ответственность за общее состояние портфеля. Этот трек менее glamorous, чем acquisitions, но во многих компаниях оплачивается чуть выше.

Похожие статьи

Распространённое заблуждение: многие считают, что именно команда acquisitions управляет компанией. На самом деле во многих фирмах команда asset management крупнее — ведь компания покупает горстку сделок в год, но обязана управлять всем, чем уже владеет, непрерывно.

Капитальная сторона: работа с инвесторами и привлечение капитала

Третья ключевая функция — та, которая вообще не касается недвижимости. Кто-то должен привлекать деньги.

В небольших компаниях это одна совмещённая роль, нередко принадлежащая основателю. В крупных — она разделяется на две. Привлечение капитала (capital raising) обращено в будущее: изучение потенциальных инвесторов, подготовка питч-деков и закрытие обязательств по следующему фонду или сделке. Работа с инвесторами (investor relations) — это текущая сторона: написание квартальных и годовых отчётов, проведение апдейт-колов и ежегодных конференций для инвесторов, рассылка уведомлений о приобретениях и продажах, информирующих LP. Младшие специалисты этого направления большую часть времени готовят старших партнёров к встречам с инвесторами и превращают результаты портфеля в нечто, что LP сможет прочитать за пять минут.

Именно эта функция за последние несколько лет изменилась больше всего. Привлечение капитала прежде считалось рутиной бэк-офиса. Теперь оно на первом плане — потому что на сжатом рынке капитала повторный чек получают те компании, которые отчитываются чётко и общаются с инвесторами профессионально. То, что раньше было вопросом бэк-офиса, стало вопросом фандрайзинга.

Бэк-офис: фондовый учёт, администрирование и комплаенс

За всем этим стоит механизм, который обеспечивает законность и платёжеспособность фонда. Фондовый учёт формирует цифры: главную книгу, NAV, расчёт waterfall и финансовую отчётность. Администрирование фонда упаковывает эти цифры и ведёт операции, обращённые к инвесторам: capital calls и дистрибуции, подготовку K-1, подписные документы и ежегодную координацию аудита. Комплаенс занимается проверками KYC и AML, верификацией статуса аккредитованного инвестора и регуляторными отчётами, которых становится всё больше с момента ужесточения требований FinCEN.

Значительная часть компаний полностью отдаёт этот уровень на аутсорсинг. Сторонний администратор фонда ведёт учёт, обслуживает инвесторов и фактически заменяет часть или весь внутренний бухгалтерский блок. Логика проста: четырёхчеловечный спонсор не может обосновать содержание штатного CFO, фондового бухгалтера и офицера по комплаенсу — поэтому он их арендует. Компромисс — контроль и гибкость в обмен на стоимость и репутацию; при этом институциональные LP нередко предпочитают независимый надзор, который сигнализирует о привлечении внешнего администратора. Подробнее об этом решении — в нашем руководстве по администрированию фондов.

Карьерная лестница и вознаграждение на каждой ступени

Карьерная лестница в компании по управлению недвижимостью в сфере private equity повторяет общий путь private equity с рядом особенностей. Ступени выглядят примерно так: аналитик (Analyst), ассоциат (Associate), иногда старший ассоциат (Senior Associate), вице-президент (Vice President), директор (Director) или старший вице-президент (Senior Vice President), затем — принципал (Principal), управляющий директор (Managing Director) или партнёр (Partner) на вершине. Уровней здесь меньше, чем в традиционном PE, и старших позиций меньше, что делает продвижение медленным и сложным. Карьера строится внутри того трека, на котором Вы работаете: ассоциат acquisitions движется к старшей роли в acquisitions, а не переходит в asset management.

Картина вознаграждений, составленная по данным Glassdoor и отраслевых исследований, выглядит примерно следующим образом. Аналитик в сфере управления коммерческой недвижимостью зарабатывает в среднем около $108 000, а наиболее высокооплачиваемые специалисты — свыше $180 000. Инвестиционный аналитик в сфере недвижимости в среднем — около $137 000. Аналитики по acquisitions — около $100 000–$102 000. На уровне VP медианное совокупное вознаграждение вице-президента по acquisitions составляет $229 000–$261 000. На уровне топ-менеджмента специалисты с двадцатилетним институциональным опытом получают базовый оклад около $250 000–$450 000, а совокупное вознаграждение с учётом бонусов и стимулов достигает $500 000–$900 000.

На эти цифры больше всего влияют два фактора, а не сама должность. Во-первых, вознаграждение в этой отрасли существенно смещено в сторону бонусов, а на старшем уровне — в сторону carried interest (доля в прибыли от сделок, выплачиваемая при успешной продаже активов). Два человека с одинаковыми должностями могут зарабатывать совершенно по-разному в зависимости от результатов их сделок. Во-вторых, Ваша ценность определяется «зрелостью» сделок — числом закрытых транзакций. Чем больше сделок за плечами, тем больше доверия к Вашим допущениям и тем выше Ваши требования — именно поэтому специалисты нередко оказываются привязаны к определённому типу объектов и географии.

Востребованные квалификационные обозначения концентрируются вокруг нескольких аббревиатур: CFA, CCIM и BOMA регулярно встречаются среди специалистов по asset management и инвестициям.

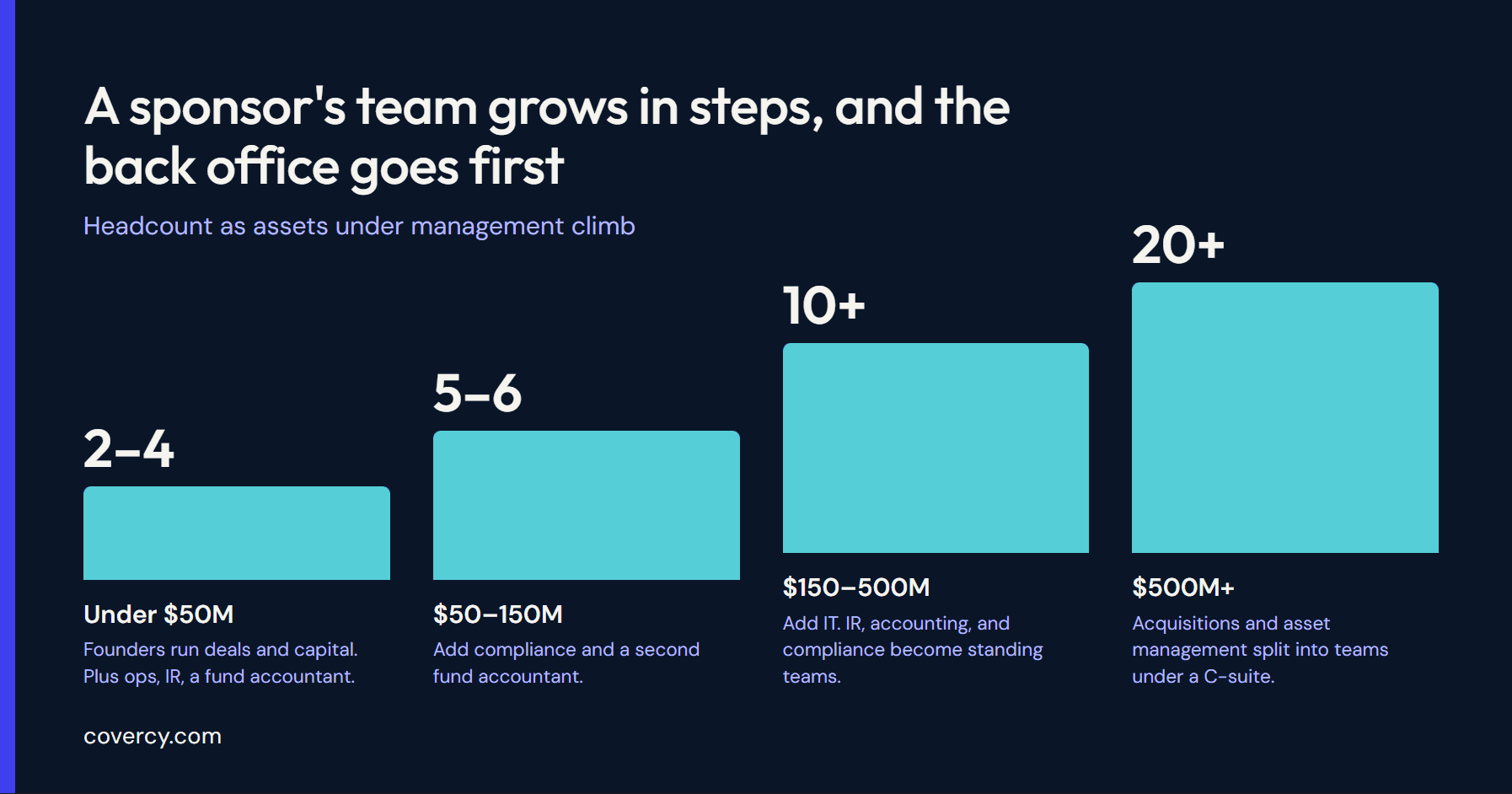

Масштабирование команды в зависимости от активов под управлением

Вот что обычно упускается в большинстве описаний органиграмм. Структура не является фиксированной. Она расширяется вполне предсказуемыми шагами по мере роста привлечённого капитала, и эти шаги привязаны к AUM и числу инвесторов.

При AUM примерно до $50 млн и менее 75 инвесторов компания, как правило, работает силами двух-четырёх штатных сотрудников: фондового бухгалтера, операционного менеджера и специалиста по investor relations, тогда как основатели сами занимаются acquisitions и привлечением капитала. В диапазоне $50–$150 млн и до 150 инвесторов компания обычно добавляет нескольких специалистов — нередко офицера по комплаенсу и второго фондового бухгалтера, — потому что нагрузка по отчётности и регулированию превысила возможности одного человека. При AUM свыше $150 млн и более 150 инвесторов компании начинают нанимать IT-специалиста и формировать investor relations, бухгалтерию и комплаенс как полноценные команды, а не отдельные ставки. На институциональном масштабе — свыше примерно $500 млн — acquisitions и asset management превращаются в самостоятельные команды под руководством C-suite в составе директора по инвестициям, финансового директора и операционного директора.

Общая закономерность неизменна. Небольшие компании защищают фронт-офис и отдают всё остальное на аутсорсинг или сжимают. Рост проявляется прежде всего в найме бэк-офисных специалистов — именно туда приходится нагрузка при увеличении числа инвесторов.

Реальность большинства компаний: работа в режиме экономии

Аккуратная органиграмма с поимённо названными департаментами описывает меньшинство рынка. Большинство спонсоров — небольшие компании. Один участник форума — инвестиционный аналитик из компании по управлению недвижимостью в сфере private equity — описал фонд с двумя VP, одним ассоциатом и собой, отметив, что потока сделок недостаточно для поддержки команды из четырёх человек. Когда портфель оказался в состоянии дистресса, половина команды ушла. Это и есть реальный облик значительной части отрасли: несколько человек, каждый из которых носит несколько шляп, без запаса прочности на случай ухудшения условий.

Для соло-синдикатора или партнёрства из двух человек основатель является одновременно руководителем по acquisitions, привлечению капитала, контактным лицом по investor relations и тем, кто подписывает чеки на выплату дистрибуций. Специализация — это роскошь, которая приходит с масштабом. Тем не менее знание полной органиграммы важно даже для таких компаний: оно подскажет, от какой шляпы отказаться первой, когда наконец появится возможность нанять сотрудника.

Технологический стек: три уровня, а не один инструмент

Спросите GP, какое программное обеспечение они используют, — и редко получите один ответ. Стек делится на три уровня, и путаница между ними — распространённая и дорогостоящая ошибка.

Первый уровень — управление сделками и пайплайном. Здесь живёт acquisitions: финансовое моделирование в Excel и ARGUS, а также CRM для отслеживания брокерских отношений и пайплайна сделок. Активные покупатели, ведущие 20 и более сделок в год, как правило, переходят на специализированный инструмент управления пайплайном или конфигурацию Salesforce; наиболее высокообъёмные институциональные покупатели добавляют полную интеграцию с инструментами андеррайтинга. Небольшие компании часто начинают с адаптации универсального CRM под свои задачи.

Второй уровень — управление недвижимостью: операционное и учётное программное обеспечение для самих объектов. Эти платформы обеспечивают сбор арендных платежей, лизинг, техническое обслуживание и учёт на уровне объекта. Они превосходно справляются с управлением недвижимостью, но никогда не создавались для фандрайзинга. Компании, которые пытаются растянуть систему управления недвижимостью на коммуникации с инвесторами и waterfall-расчёты, в итоге надстраивают поверх неё электронные таблицы — именно там и появляются ошибки.

Третий уровень — управление инвестициями и инвесторский портал, созданный специально для отношений GP–LP: привлечение капитала, онбординг инвесторов, подписные документы, расчёт waterfall, дистрибуции, доставка K-1 и отчётность об эффективности — всё в одном брендированном портале. Внедрение этого уровня стало массовым: сотни тысяч LP управляются через такие платформы, а ценовой диапазон широко варьируется в зависимости от того, ориентирован ли инструмент на начинающего синдикатора или на институционального управляющего.

Два тренда сейчас перестраивают этот уровень. Первый — проникновение AI в рабочий процесс: составление писем с обновлениями для инвесторов, извлечение данных из PPM и предложительных документов, скоринг сделок, сокращение времени подготовки отчётов с недель до часов. Второй — консолидация. GP устали связывать CRM, систему управления недвижимостью, электронные таблицы и email-переписку во что-то, напоминающее бэк-офис, и переходят на платформы, замыкающие цикл между банкингом, капиталом и отчётностью для инвесторов. Когда дистрибуции проходят через ту же систему, где хранятся средства, банковская выписка становится отчётом о дистрибуциях. Именно в этом направлении движется вся категория.

Структура следует за капиталом и доверием

Организационная структура инвестиционной компании в сфере недвижимости — это карта того, что она ценит и где сосредоточены её риски. Фронт-офис покупает активы и управляет ими. Капитальная сторона привлекает деньги и удерживает инвесторов. Бэк-офис следит за корректностью цифр и чистотой отчётности. По мере роста компании эти функции разделяются на отдельные команды; по мере сокращения или на старте — снова концентрируются на нескольких людях. Технологии либо закрепляют эти разделения с помощью разрозненных точечных инструментов, либо объединяют их в единый рабочий процесс. Для небольшого GP, решающего, что строить самому, что отдавать на аутсорсинг, а что покупать, — изучение полной органиграммы заранее является самым дешёвым планированием, которое может себе позволить основатель.