Nir Biton

Continuous rate – the rate at which the U.S. dollar trades against the shekel; the rate changes every moment (every millisecond).

The currency pair (USD–ILS) is traded as long as there is a value day for the Bank of Israel (for example, on Yom Kippur there is no trading in the shekel and therefore the rate does not change). An additional condition is trading in the dollar; if on that day there is no trading in the dollar (Sundays), there will be no USD/ILS trading.

Therefore, the continuous rate is a rate that changes every moment from the night between Sunday–Monday until Friday evening (U.S. time).

The continuous rate changes 24 hours a day, starting from trading hours in New Zealand and Australia until the end of trading on the U.S. West Coast.

Of course, during trading hours in Israel, USD/ILS trading will be the liveliest, though not necessarily the most volatile.

What determines whether the continuous rate will rise or fall? Market forces alone!

If there is demand—the rate will rise; if there is no demand, the rate will likely fall (or not change).

Representative rate – the rate set by the central bank in Israel (Bank of Israel) according to a formula that calculates fluctuations and prices between 13:15–15:15; it is published every day at 15:30.

Why do we need a representative rate? To compare apples to apples. What do we mean—can I say that today compared to yesterday the USD/ILS rate went up or down? Compared to what time? It may be that today at 09:00 the USD/ILS rate was higher than yesterday at 16:00, while at 19:00 today it was lower than yesterday at 02:45. Confused? So are we.

How will we know? We’ll compare the rate at 15:30 to the rate at 15:30 day after day, or in short, compare the representative rates set by the Bank of Israel. That will be our indication of whether the USD/ILS exchange rate rose or fell compared to yesterday.

The representative rate means nothing beyond that; do not attribute too much importance to it.

One important note—the Bank of Israel tends to intervene in Israel’s FX market by purchasing dollars on the interbank FX market.

What does that mean? In order to raise the USD/ILS rate, the Bank of Israel turns to local banks (Leumi/Poalim/Discount, etc.) and buys dollars from them.

What happens next? The banks are short dollars and need to buy them back—only at a higher price.

Why higher? Because demand is higher—after all, the Bank of Israel does not buy $10,000,000 but much larger amounts—$300,000,000 and more. Thus the Bank of Israel effectively intervenes in determining the dollar–shekel rate as it sees fit.

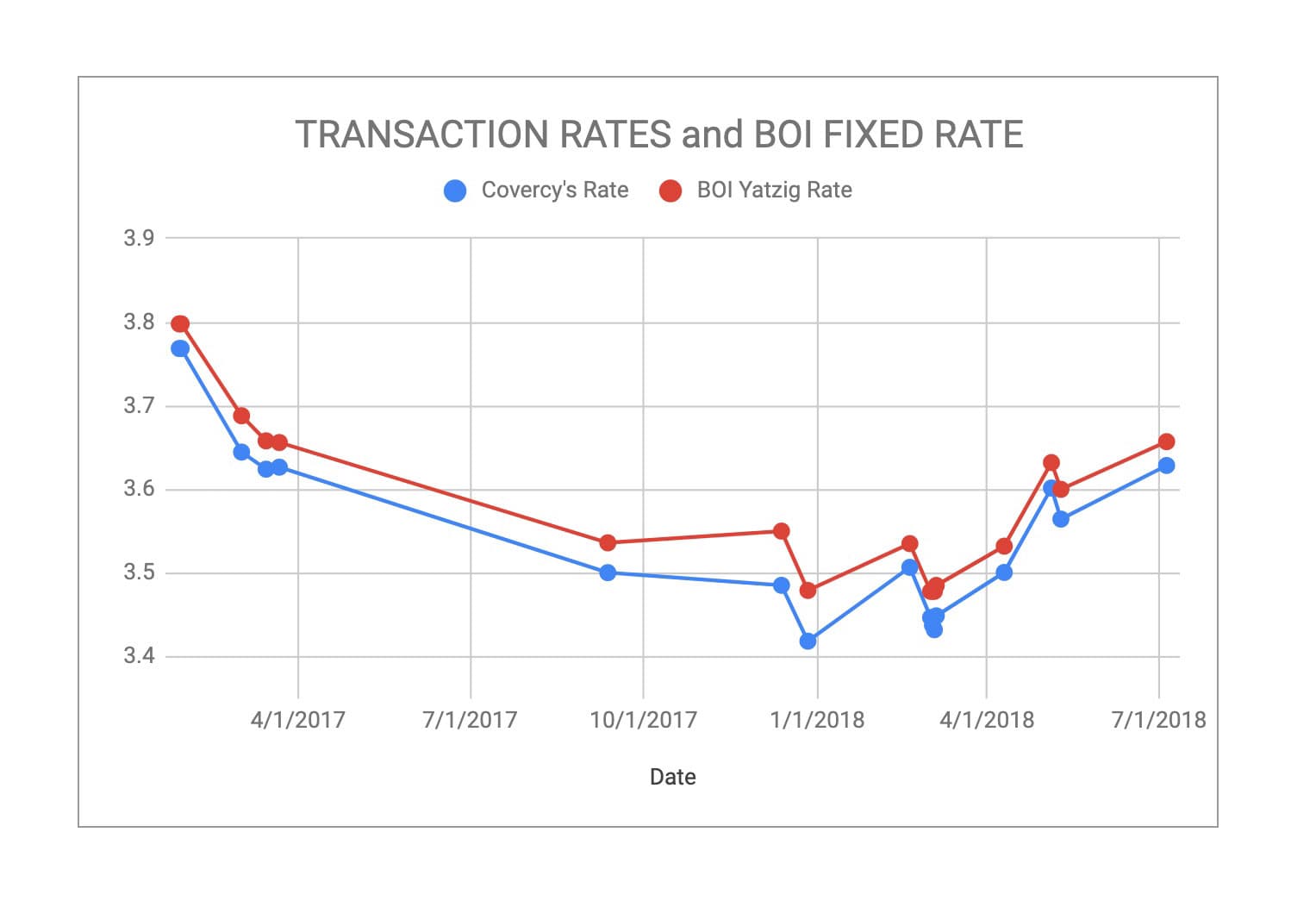

We checked this – we took all Covercy transfers in 2017 and early 2018 in USD, which of course are executed at the continuous rate (subject to market forces), and compared them with the representative rate on the same trading day (all continuous rates based on transfers that day versus the representative rate that same day).

And what did we find? In 60% of the cases the representative rate was higher than the continuous rate—and not just marginally. On average, whenever the representative rate was higher than the continuous rate, it was higher by 0.2%. Conversely, when the representative rate was lower than the continuous rate, it was lower by only 0.0004% on average.

This result is biased in favor of the representative rate, likely due to Bank of Israel intervention in the market.

Therefore, statistically, buying dollars at the representative rate will be more expensive than buying dollars at the continuous rate.