Understanding the capital stack in commercial real estatecommercial real estate

Read on for a comprehensive guide covering the ins and outs of the commercial real estate capital stack: financing & fundraising, the debt-to-equity split, risk levels, exit strategies, and more.

Covercy is trusted by:

Everything you need to know about the capital stack in commercial real estate

But first: what is the capital stack?

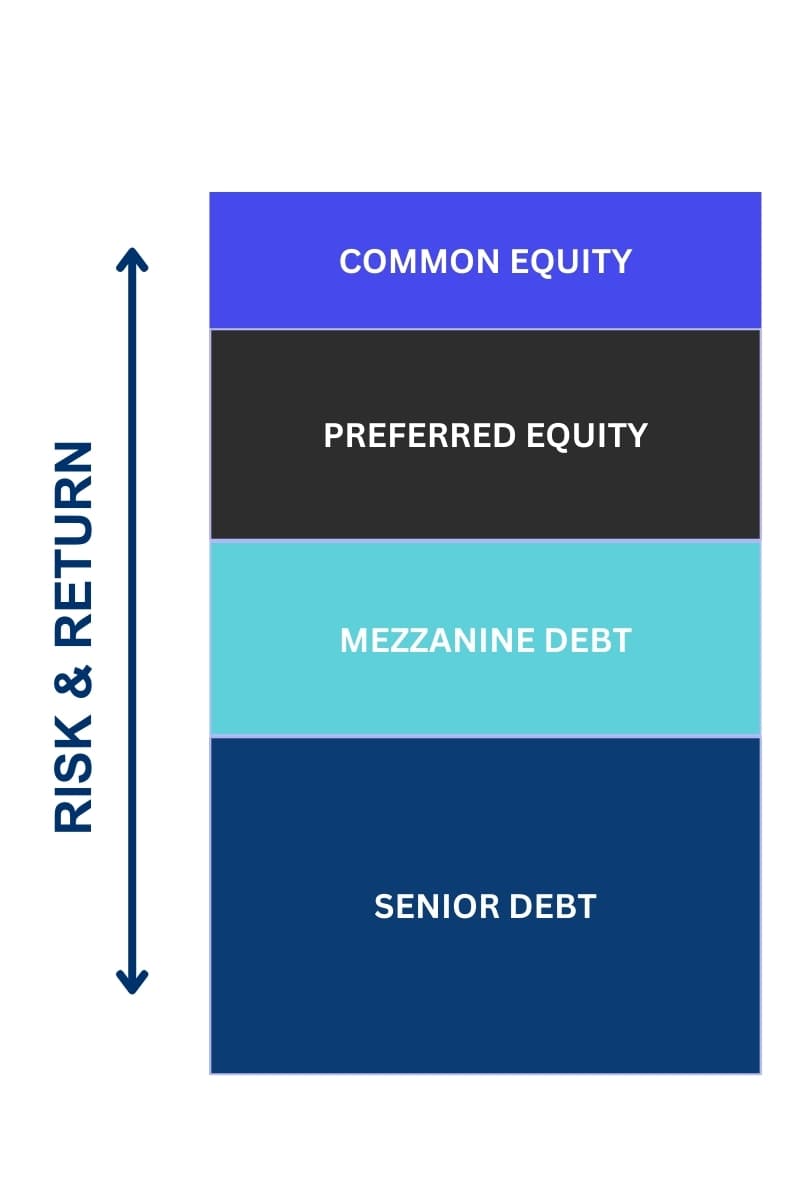

The capital stack in real estate refers to the layered structure of financing sources used in a property investment. It typically (but not always!) includes senior debt, mezzanine debt, preferred equity, and common equity, each representing different levels of risk, return, and priority in the event of income distribution or liquidation.

This particular structure is popular with General Partners (GPs) and their syndicated investors because of its balanced approach to risk and return. Senior debt is less risky, so it forms the base of the capital stack, providing a solid foundation. As you move up the stack, the risk and potential return increase. This allows different types of investors, with varying risk appetites, to participate in the real estate investment. The diversification across different levels of risk and return is what makes this structure appealing and widely adopted.

Senior Debt

Lowest Risk • Fixed Return • First Priority

Mezzanine Debt

Moderate Risk • Higher Fixed Return

Preferred Equity

Higher Risk • Preferred Returns

Common Equity

Highest Risk • Highest Potential Return

Senior Debt

The senior debt typically makes up 50-70% of the total capital stack. This is the largest portion and includes the primary mortgage or loan. It holds the first lien position, meaning it has the highest priority for repayment in the event of a default or liquidation of the property. This priority position is often secured by a mortgage or a deed of trust on the property.

The primary use of senior debt is to finance a significant portion of the purchase price or the cost of developing a property. It's the foundational layer of financing that allows investors and developers to leverage their capital and undertake large-scale real estate projects. Since senior debt must be serviced first, it has a direct impact on the property's cash flow. Investors and property managers need to ensure that the property generates enough income to cover these debt service obligations.

Mezzanine Debt

The mezzanine debt often comprises about 10-20% of the total capital stack. This is a subordinate debt that sits beneath the senior debt but above equity within the capital stack. It is usually secured with a pledge of the equity of the borrowing entity, not the real estate asset itself. This means that in the event of a default, the mezzanine lender can potentially take control of the entity that owns the property.

Mezzanine financing often involves more flexible terms than senior debt, including the potential for interest to be accrued (added to the loan balance) or paid-in-kind (PIK), allowing the borrower to defer cash interest payments. And sometimes, mezzanine loans include options to convert debt into equity, allowing lenders to participate in the upside potential of the property.

Preferred Equity

Preferred equity sits above all forms of debt but below common equity in the capital stack. This means that in the event of a default or liquidation, preferred equity holders are paid out after all debt obligations have been met but before any distributions are made to common equity holders.

Preferred equity investors generally receive regular dividend payments, which can be fixed or variable. These payments usually have priority over distributions to common equity holders, making it a relatively stable income source. The terms, such as dividend rate, payment schedule, and maturity date, are negotiated between the issuer and the investors. These terms often include features like conversion rights (to common equity), participation in upside potential, and specific financial covenants.

Preferred equity often comes with an "equity kicker," which is an additional return component, usually tied to the performance of the real estate asset. This kicker can enhance returns if the property performs well.

Common Equity

Common equity is at the bottom of the capital stack. This means it bears the highest level of risk because common equity holders are the last to be paid in the event of income distribution or property liquidation, after all debts and preferred equity obligations have been fulfilled.

Due to its position, common equity is the riskiest form of investment in the capital stack. However, it also offers the potential for the highest returns. The returns on common equity are directly linked to the performance of the real estate asset, including value appreciation and rental income. Common equity is primarily raised from investors who contribute capital in exchange for an ownership stake in the property. These investors can range from individual investors and real estate investment trusts (REITs) to institutional investors.

Common equity is crucial for balancing the capital stack and ensuring that a project has enough capital to proceed. It often represents the commitment of the principal investors and can be a key factor in securing other forms of financing.

Manage your commercial real estate capital stack with Covercy.

Unlike most investment management software on the market, Covercy approaches commercial real estate syndication with a unique focus on the financial and funding side.

Starting with customizable waterfall structures and ending with GP and LP bank accounts opened right within the platform, capital contributions and distribution payments can be transferred seamlessly to and from accounts with the click of a button.

Meanwhile, uninvested and uncalled idle capital generates high interest for the syndicator, LP, or project, depending on your specific deal structure.

The Debt-to-Equity Split & Risk Tolerance

The debt-to-equity split in commercial real estate is a critical decision that impacts the overall risk and return profile of an investment. Typically, this ratio represents the balance between borrowed funds (debt) and directly invested capital (equity) in financing a property. Common ratios vary, but a conventional split might be in the range of 75:25 or 70:30 debt-to-equity. This implies that for every $100 invested in a property, $70-$75 comes from debt and $25-$30 from equity.

The higher the debt proportion, the greater the leverage. Leveraging can amplify returns on equity, as it allows for the purchase of a more valuable property with the same amount of equity. However, it also increases risk, particularly in volatile markets or downturns. If a property's value decreases or if it fails to generate expected income, the debt obligations still remain, which can disproportionately affect equity returns. Conversely, a lower debt-to-equity ratio means less leverage, resulting in lower potential returns but also lower risk, as the investment is less sensitive to market fluctuations and interest rate changes.

GPs make decisions about the debt-to-equity split by carefully weighing the risk tolerance of their investment strategy, the specifics of the property, and the market conditions. They consider factors like the property's location, type, and potential for income generation, as well as broader economic indicators like interest rates and real estate market trends.

Capital Stack Best Practices

For commercial real estate GPs, structuring the capital stack is a crucial step in the investment process. Here are six best practices to consider:

Comprehensive Market Analysis

Before structuring the capital stack, GPs should conduct an in-depth market analysis. This includes understanding the local real estate market trends, assessing property values, and analyzing the economic and demographic factors that could impact the investment. This groundwork helps in making informed decisions about the type and amount of financing required.

Risk Assessment and Return Objectives

GPs should clearly define their risk tolerance and return objectives. This involves understanding the risk-return profile of different layers of the capital stack and matching them with the investment goals. For instance, a higher proportion of equity might be preferred for a high-risk, high-return project, while a project with stable, long-term returns might be more heavily financed with debt.

Diversified Financing Sources

Diversification isn't just important for investments; it's also crucial in financing. GPs should explore various financing options, including traditional bank loans, mezzanine financing, preferred equity, and common equity. Each source has different terms, costs, and flexibility, and a well-balanced mix can optimize the capital structure.

Strong Lender and Investor Relationships

Building and maintaining strong relationships with lenders and investors is vital. This not only helps in securing favorable terms but also in ensuring smooth transactions and potential future opportunities. Transparent communication and regular updates about the project can foster trust and reliability.

Flexibility and Contingency Planning

The real estate market is dynamic, and GPs should structure the capital stack with enough flexibility to adapt to changing market conditions. This might include negotiating terms that allow for refinancing or restructuring if needed. Additionally, having contingency plans in place for scenarios like market downturns or unexpected expenses can safeguard the investment.

Compliance and Legal Diligence

Ensuring compliance with legal and regulatory requirements is crucial. This involves understanding and adhering to securities laws, real estate regulations, and other legal frameworks relevant to the financing structure. Engaging with legal and financial advisors early in the process can help navigate these complexities.

Tips for finding additional investors for your common equity layer

Typically, the financing structure is planned and partially secured before finalizing a property purchase. This preliminary approval for financing gives GPs the confidence to move forward with property acquisitions.

If a GP is struggling to complete the common equity portion of the capital stack, they can explore several avenues to find additional Limited Partners (LPs):

Networking and Industry Events

Attending real estate investment conferences, local meetups, and networking events can help GPs connect with potential investors.

Partnerships with Investment Firms

Collaborating with investment firms or real estate funds that have access to a pool of investors can be beneficial.

Crowdfunding Platforms

Real estate crowdfunding platforms can provide access to a wide range of investors interested in smaller equity contributions.

Marketing and Promotion

Effective marketing strategies, including digital marketing and presentations to investment clubs, can attract potential LPs.

In terms of other creative financing options:

Seller Financing

In some cases, the seller of the property might be willing to finance the sale, which can be an alternative to traditional bank financing.

Joint Ventures

Forming a joint venture with another investor or investment firm can provide additional capital and share the risk.

Government Grants and Incentives

In certain areas, government programs might offer grants or incentives for real estate development, particularly for projects that include affordable housing or urban revitalization.

Leaseback Arrangements

In a leaseback, the GP sells the property and then leases it back from the buyer, which can free up capital while maintaining control over the property.

Each of these strategies has its own set of advantages and considerations, and the choice depends on the specific circumstances of the investment and the GP's overall strategy.

When to Restructure Your Capital Stack

GPs might consider restructuring the capital stack under several conditions, often driven by changes in the market, the performance of the property, or the investment objectives. Restructuring the capital stack can be a strategic move to align the investment with current conditions and goals, but it can also involve costs and complexities.

Changes in Market Conditions

A commercial real estate General Partner (GP) should consider restructuring the capital stack when there are significant changes in market conditions that affect the investment's profitability or risk profile. For instance, if interest rates have decreased substantially since the initial financing was secured, refinancing existing debt at lower rates could reduce interest expenses and improve cash flow. Alternatively, if the real estate market has strengthened, the increased value of the property might provide an opportunity to secure more favorable loan terms or attract additional investors.

Shift in Property Value or Performance

Restructuring may also be appropriate when the performance of the property itself changes. If a property's value appreciates due to successful management, development, or changes in the local market, the GP might leverage this increased equity. This can be done by taking on additional debt against the property's higher value, thus altering the debt-to-equity ratio in favor of a more optimal capital structure. Similarly, if a property is underperforming, restructuring might involve renegotiating loan terms or bringing in new equity partners to provide additional capital for improvements.

Investment Strategy Changes

A shift in the investment strategy or the nearing of loan maturities can prompt a capital stack restructuring. GPs might adjust their strategy in response to changing investor preferences or economic conditions, moving from a high-leverage, high-risk approach to a more conservative one, or vice versa. Also, as loans reach maturity, refinancing them can help align the capital structure with the current market and investment conditions. However, GPs must carefully weigh the costs, such as refinancing fees and potential impacts on existing investors, against the benefits of restructuring.

Investment management software designed with commercial real estate syndication in mind

Covercy is the first real estate platform where banking meets investment management.

Bringing capabilities such as investment management, fundraising, automated distributions, and more into a single platform, Covercy also provides GPs and their teams with the ability to service a high volume of outside investors in a single platform. Syndicators can also open, manage, track, and report on bank accounts and activity tied to their assets, funds, investors, and more.

More capital stack resources

Tailor Covercy's commercial real estate syndication software for your firm

Tailor Covercy's investment management software for your real estate firm

Fundraising Starter

For raising your next deal

- CRM

- Investor Portal

- Fundraising

- Distributions

- Reporting

- Funds & Capital Calls

- Integrations

- Valuations

- Retail & Broker-Dealer

- Accounting & Compliance

Standard

For managing capital you've already raised

- CRM

- Investor Portal

- Fundraising

- Distributions

- Reporting

- Funds & Capital Calls

- Integrations

- Valuations

- Retail & Broker-Dealer

- Accounting & Compliance

Professional

The full platform: funds, deals, payments, integrations

- CRM

- Investor Portal

- Fundraising

- Distributions

- Reporting

- Funds & Capital Calls

- Integrations

- Valuations

- Retail & Broker-Dealer

- Accounting & Compliance

Fund Administration

Add when you need NAV, fund accounting, or retail raising

- CRM

- Investor Portal

- Fundraising

- Distributions

- Reporting

- Funds & Capital Calls

- Integrations

- Valuations

- Retail & Broker-Dealer

- Accounting & Compliance

Ready to optimize your capital stack?

Join thousands of real estate professionals who trust Covercy

Get Started with Covercy (opens in a new tab)