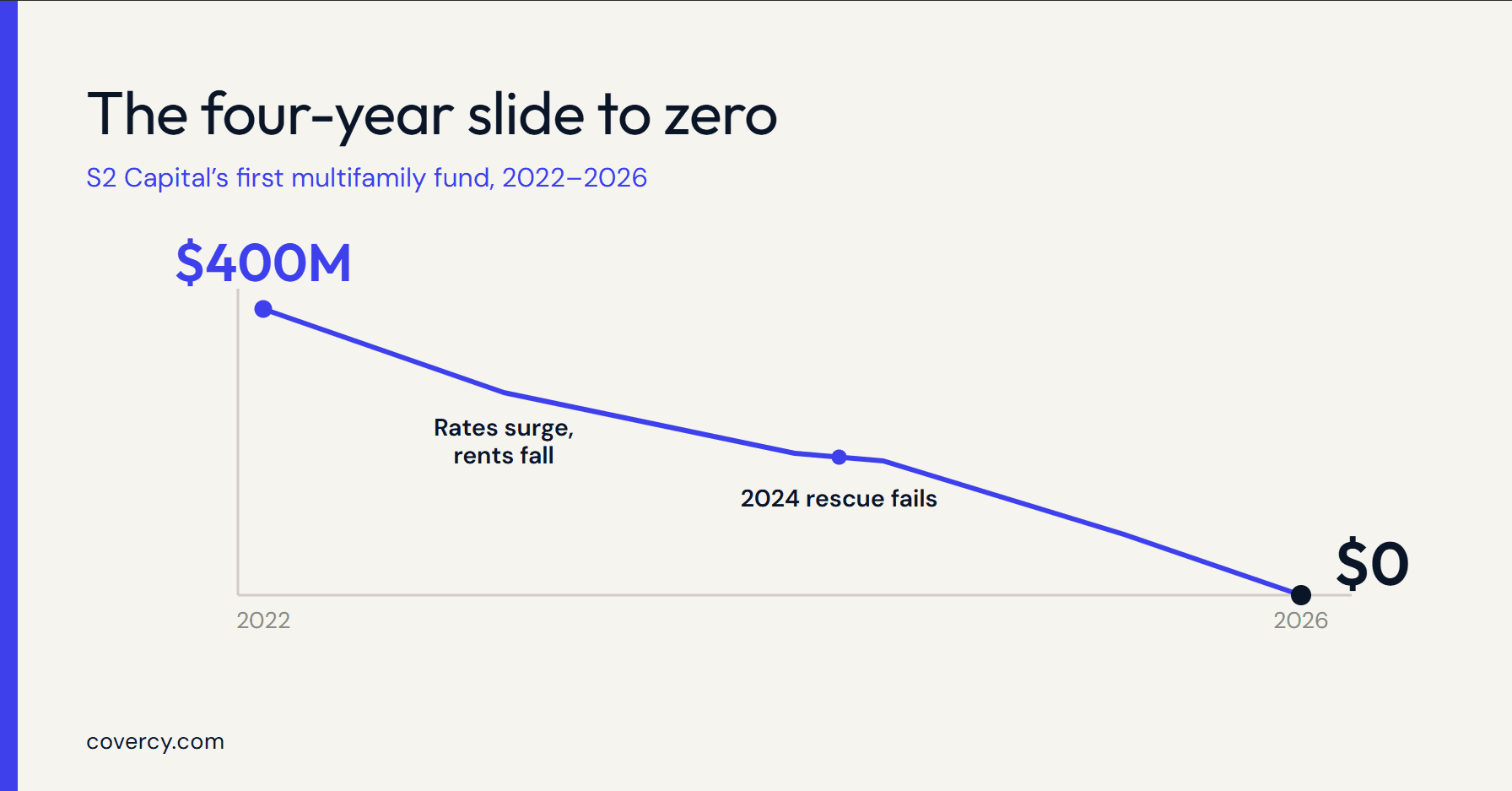

On July 1, Scott Everett, the founder of S2 Capital, sent his limited partners a letter no general partner (GP) wants to write. The firm's first value-add multifamily fund, which raised $400 million and held 20 properties, will return no capital. Limited partners and preferred equity investors get nothing back. For every LP reading that letter, it forces the question they can rarely answer between quarterly reports: what is actually happening to my money?

The fund closed in 2022 at a $400 million hard cap, comfortably past its original $250 million target. The causes of what followed are familiar to anyone operating value-add multifamily across the Sun Belt. Over the life of the fund, operating expenses rose an average of 16% and interest costs climbed roughly 50%, while rents fell 24%, according to reporting from CRE Daily. The fund carried floating-rate debt through the cheap-money years, and when rates jumped the coverage math gave way. Everett now plans to buy the debt on the fund's viable assets, restructure it, and move those properties into a new vehicle to recover what he can, per the July 1 letter reported by The Real Deal.

Leverage broke the fund. Reporting shapes the aftermath.

This is a leverage story first. No investor reporting software refinances a floating-rate loan or grows rents in a soft market. But the same reporting flags a shift on the investor side: LPs are now examining debt structures, rate exposure, and capital reserves far more closely before they commit to a fund. That scrutiny builds over years of quarterly statements. It does not begin the day a distribution stops.

Fund administration is where trust is won or lost

A multifamily fund lives or dies on the quality of its books. Capital accounts have to reconcile. NAV has to be defensible. Distributions and capital calls have to tie back to the exact numbers investors see in their statements. When a fund hits trouble the way S2's did, the firms that hold their investors' confidence are the ones whose fund administration stayed clean and current the whole way through. Books reconstructed in a hurry once the losses land tell investors the operation was never really in control.