The Complete Guide to Investor Portals: Features, Types & How to Choose | Covercy

Investor Management·18 min read

The Complete Guide to Investor Portals: Features, Types & How to Choose

An investor portal is no longer a place to park PDFs — it's where investors check performance, get paid, and decide whether they'll invest again. Here's what a modern portal does, the types available, and how to choose one.

Kristen Erickson··18 min read

Ask ten fund managers what an investor portal is and most will describe a place to store documents — a digital filing cabinet where investors can download a K-1 or a quarterly report. That definition is a decade out of date. A modern investor portal is the surface your limited partners (LPs) actually experience your firm through: it's where they check how an investment is performing, see a distribution hit their account, respond to a capital call, and decide — quietly, every quarter — whether they'll commit to your next deal.

This guide is for general partners (GPs), sponsors, and fund managers who are evaluating an investor portal — whether you're moving off spreadsheets and email for the first time or replacing a portal that has become a glorified document folder. We'll cover what an investor portal actually does, the different types on the market, the features that separate a modern portal from a static repository, and a practical framework for choosing one. The focus throughout is commercial real estate (CRE), but the principles apply to any private-capital manager raising from non-institutional investors.

Why Investor Portals Matter Now

The bar for investor experience has moved. The same LPs who invest in your syndications and funds also check their brokerage balance on their phone, get instant payment confirmations from their bank, and expect a real-time answer to almost any financial question. When they invest with a GP and then have to email an associate to ask what their distribution was last quarter, the contrast is jarring. The portal is where that contrast is either resolved or reinforced.

For the GP, the stakes are operational as much as they are about perception. Investor relations on email and spreadsheets has a ceiling. Every distribution detail request, every "can you resend my K-1," every "what's my remaining commitment" is a manual task that scales linearly with the number of investors. A firm with 30 LPs can absorb that. A firm with 300 cannot. The hidden cost of running investor relations out of an inbox isn't just time — it's the errors that creep in when the same numbers are copied between a spreadsheet, an email, and a PDF, and the trust that erodes when an investor catches one.

An investor portal addresses both sides at once. It gives LPs self-service access to the information they would otherwise have to ask for, and it gives GPs a single place where that information lives, stays current, and is shown to each investor according to what they're actually entitled to see. The payoff is two-sided: less operational burden for the GP, more transparency for the LP, and — over time — the kind of professional experience that makes investors comfortable writing the next check.

Related Articles

What an Investor Portal Actually Does

Before comparing products, it helps to be precise about the core jobs a portal performs. Most portals cover some version of four areas: a performance dashboard, document and tax delivery, reporting, and communications. The depth of each is where products diverge.

Dashboard and Performance

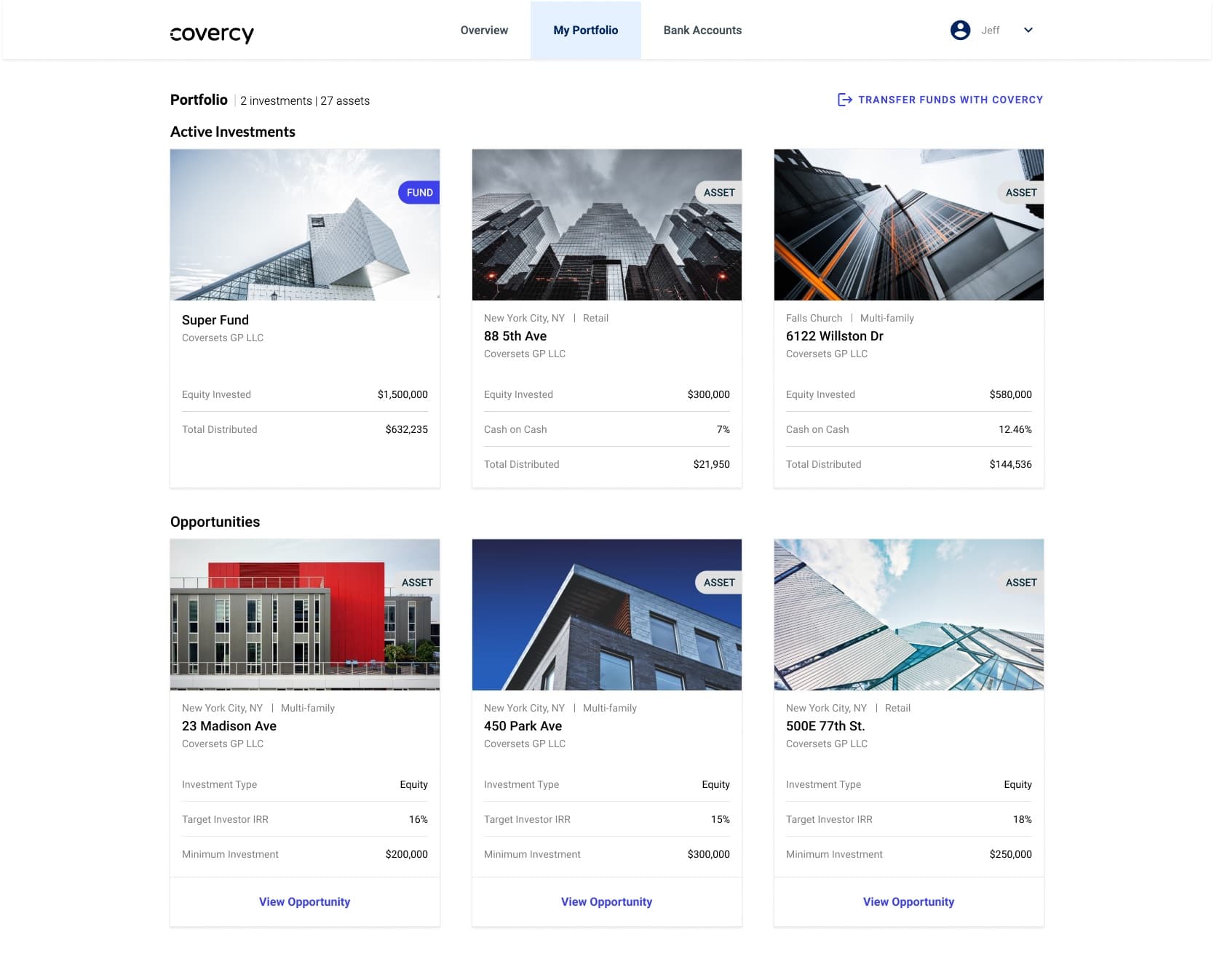

The dashboard is the LP's home screen, and it sets the tone for everything else. A good one answers the questions an investor actually has at a glance: how much have I committed, how much have I contributed, how much capital is still uncalled, and how much have I been distributed. In a strong portal those headline figures sit above a portfolio view — a map of the holdings an investor is in, a cash-flow chart over time, and a card for each investment showing its commitment and distribution progress.

The detail that matters here is honesty of representation. Progress toward a commitment isn't a single number — it's the split between what's been contributed, what's been called but not yet paid, and what remains uncalled. A portal that shows that breakdown as a stacked progress bar, with the figures available on tap or hover, tells the investor the truth of where they stand. A portal that flattens it into one percentage is hiding information the investor will eventually ask for anyway.

Documents and K-1s

Document delivery is the feature every portal claims and few do well. The hard part isn't storage — it's access control. An investor should see exactly the documents tied to their positions and nothing else, and that scoping has to hold up across a firm with multiple holdings, multiple share classes, and investors who hold different things in different deals. The right model lets a GP share a document at the level that makes sense — to everyone in a holding, to a specific share class, or to an individual position — and have the portal show it to precisely the right people, with download permissions controlled separately from view permissions.

Tax documents are the highest-stakes case. K-1 season is when investors log in most, and it's when a portal earns or loses their confidence. Being able to deliver each investor's K-1 to their document center — viewable in the browser and downloadable — turns the single most predictable support spike of the year into a non-event. For more on organizing this side of the portal, see our guide on CRE investor document management.

Reporting

Reporting is where the portal stops being a passive store and becomes a communication channel. Instead of attaching a PDF to a quarterly email, a GP publishes a report into the portal, where it's tied to the right holding and visible to the right investors. A capable reporting workflow lets the GP build the report — narrative sections, financials, attachments — preview exactly how it will look, and publish it with an optional notification to investors. On the investor side, the report appears in a list scoped to their holdings, with a clean in-browser preview and a branded PDF to download.

The quality signal to look for is whether reports carry the GP's branding — logo and colors — through to the rendered PDF, and whether report access respects share-class scoping the way documents do. An investor in one class shouldn't see a report written for another. When reporting lives in the portal rather than the inbox, investors stop losing reports in email threads, and the GP gets a single record of what was published and when.

Communications

The communications view is the investor's record of what the GP has sent them — capital call notices, distribution notices, opportunity invitations, and direct messages — gathered in one place rather than scattered across an inbox. The value is continuity: an investor who changes email providers or loses a message still has the full history of communications from their investment manager in the portal. Be clear-eyed about what this is, though. A portal communications log is a system of record for what the GP has sent, not a two-way chat or a discussion forum. The honest framing is durable, scoped delivery of the messages that matter, not a social feed.

The Features That Separate Modern Portals From File Cabinets

Here's the test that separates a real investor portal from a branded document folder: can an investor get paid through it, fund a capital call through it, and manage the bank account that money moves to — all without leaving the portal? In most products the answer is no. Distributions still run through a separate bank portal and a spreadsheet, and the "portal" only shows a PDF after the fact. The portals worth paying for are the ones where the money movement itself lives in the same system the investor logs into.

Bank account management is the foundation. A modern portal lets an investor link a bank account — connecting it instantly through a provider like Plaid, or entering it manually — set a default account, and assign accounts to specific positions. Because banking details are sensitive and consequential, changes route through a GP approval workflow rather than taking effect silently: when an investor adds or changes an account, the GP reviews and accepts the request, and the system prevents a distribution from being finalized while a banking change is still pending. That's the difference between a portal that displays information and one that's trusted to handle money.

On the inflow side, the portal should let an investor fund a capital call directly — initiating an ACH debit from a linked account, or getting wire instructions generated as a branded PDF when they'd rather send a wire. The investor responds to the call in the portal; they don't manage the call itself — capital calls are initiated by the GP — but the act of paying happens where the investor already is. Pair that with a cash-flows view that shows contributions and distributions over time, with the status of each call clearly labeled, and the investor has a complete, current picture of money in and money out. The distribution side of this workflow is covered in depth on our distributions page.

Two more capabilities mark a portal built for how firms actually operate. The first is multi-language support: a portal that serves investors in English, Spanish, and Hebrew — with right-to-left layout where the language requires it — is a portal built for the reality that capital is global, even for a small firm. The second is entity management: high-net-worth investors and family offices invest through LLCs, trusts, and partnerships, often several of them, and a portal should let an investor manage those investing entities and assign the right one to each position. These aren't headline features, but their absence is exactly what makes a portal feel like it wasn't built for serious investors.

“

“The test that separates a real investor portal from a branded document folder: can an investor get paid through it?”

Types of Investor Portal Solutions

"Investor portal" describes a category, not a single product shape. The right portal depends on what you manage and who your investors are. Three variants come up most often.

Private Equity Investor Portals

Private equity portals are built around the fund lifecycle: capital commitments, called and uncalled capital, distributions, and the cap-table relationships that connect investors to fund vehicles and underlying holdings. The defining requirement is the ability to represent a commitment accurately over time — contributed versus called-but-unpaid versus uncalled — and to handle investors who hold positions across multiple funds. For a PE-style manager, the portal's job is to make a multi-fund, multi-position relationship legible to an investor who might otherwise need a spreadsheet to track it themselves.

Real Estate Investor Portals

Real estate portals share the capital mechanics of PE portals but add a property dimension. Investors expect to see the assets behind their investment — location, type, and status — not just a line item. A real estate investor portal that maps holdings, shows asset-level context on each investment, and ties distributions back to specific properties speaks the language of how CRE investors think about their money. This is also the variant where deal-by-deal syndications, not just blind-pool funds, dominate: the portal has to handle a sponsor running a series of individual raises as naturally as it handles a fund.

Fund Investor Portals

Fund portals emphasize the relationship between a fund and its underlying holdings. An investor in a fund should be able to see the fund's portfolio — the holdings it's invested in — and, where they also hold a direct position, navigate to it. The reporting and document model has to respect fund structure and share classes, so that what each investor sees reflects their specific stake. For managers running both funds and direct deals, the ideal portal handles both in one investor experience rather than forcing investors into separate logins for separate structures.

The Role of CRM and Investor Relations

A portal is the investor-facing half of investor relations. The other half is the GP-facing system that decides what each investor sees, tracks the relationship, and connects the portal to fundraising. This is where a portal that's bolted onto a CRM, or a CRM with no real portal, shows its seams — and where an integrated platform pulls ahead.

The connection matters most during a raise. When a portal is part of the same system as the investor pipeline, a prospect can move from an invitation, through an accreditation step, into an application and a commitment — and the GP can watch that progression and approve investors at the right gates — without data being re-keyed between a marketing tool and an investing system. Source attribution carries through, so a GP can see which investors came from which channel. The portal and the CRM aren't two products talking to each other; they're two views of one relationship. For the fundraising side of that workflow, see our fundraising overview.

The practical lesson for evaluation: don't assess the portal in isolation. Ask how an investor gets into it in the first place, how the GP controls what each investor sees, and whether the system that raises capital is the same one that serves investors afterward. A beautiful portal fed by a disconnected back office just relocates the manual work; it doesn't remove it.

What to Look For When Choosing an Investor Portal

Most portal demos look impressive for the first ten minutes. The questions below are the ones that separate a portal you'll be happy with in year three from one you'll be migrating off. Treat them as a checklist when you evaluate.

Access control depth: can you scope documents and reports to a holding, a share class, or an individual position — and does the portal reliably show each investor only what they're entitled to?

Money movement: can investors link and manage bank accounts, fund capital calls, and receive distributions inside the portal, with GP approval on banking changes?

Accurate capital representation: does the portal show contributed, called-but-unpaid, and uncalled capital distinctly, rather than collapsing them?

Reporting workflow: can you build, preview, brand, and publish reports into the portal, with the right investors notified and scoped in?

Entity support: can investors manage multiple investing entities (LLCs, trusts, partnerships) and assign them to positions?

Onboarding and fundraising integration: is the portal connected to the system that raises capital, or is it a separate tool that needs syncing?

Investor experience details: multi-language support, mobile usability, and a dashboard that answers an investor's first questions without a support email.

Security and permissions: are permissions enforced at every level, so investors and team members see only what their role allows?

A useful framing as you score products: a portal is only as good as the data behind it. A portal that sits on top of a system already managing your investors, holdings, distributions, and banking starts with clean, current data. A portal that has to import that data from elsewhere is only as fresh as its last sync. The cost difference between the two doesn't show up in the demo — it shows up every quarter afterward.

Getting Investors to Actually Use It

Here's the part most portal evaluations skip: buying a portal and getting your investors to use it are two different projects. A portal with low adoption is worse than no portal — you've added a system to maintain and still field the same email requests, now from investors who never logged in. Adoption is a design problem and a rollout problem, and it's worth planning before you sign.

Start by removing friction at the front door. Investors should be linked to their positions automatically when they're invited, so that the first time they log in, their data is already there — not an empty shell they have to be walked through. An empty first session is the fastest way to lose an investor's interest. The portal should recognize an investor by the email the GP already has for them and connect them to everything they hold across the firm in one step.

Then give investors a reason to return, not just an invitation to visit. The events that pull investors back are financial: a distribution arriving, a capital call due, a new report published, a tax document available. A portal that notifies investors when these happen — and lands them directly on the relevant page — builds the habit. The portals with the best adoption are the ones where the most important things that happen in an investor's relationship with a GP happen in the portal, so logging in is the path of least resistance rather than an extra chore.

Finally, lead by routing real activity through the portal yourself. If you still send distribution details by email "so it's easier," investors will follow your lead and stay in their inbox. If the cleanest way to see a distribution, fund a call, or read a report is the portal, adoption follows the behavior you model. Adoption isn't a feature you buy; it's the result of making the portal the real channel rather than a parallel one.

How Covercy Approaches the Investor Portal

Covercy One was built on the premise this guide argues for: the portal is the investor-facing surface of a platform where the money actually moves, not a document folder bolted onto a CRM. Investors get a dashboard with their committed, contributed, uncalled, and distributed figures, a portfolio map of their holdings, and per-investment progress bars that show the real split between contributed, called, and uncalled capital. Documents and reports are scoped precisely — to a holding, a share class, or a position — and reports carry the GP's branding through to a downloadable PDF.

What makes it more than a viewer is the money movement. Investors link and manage bank accounts through Plaid or manually, with banking changes routed through GP approval and distributions blocked from finalizing while a change is pending. They fund capital calls by ACH debit or generate branded wire instructions, and they track every contribution and distribution in a cash-flows view. Because the portal is part of the same system that handles distributions, fundraising, and banking, the data investors see is the live data the GP manages — not an imported copy. Multi-language support, multi-entity management, and an accreditation gate for onboarding round out a portal designed for how small and mid-size firms actually serve non-institutional investors. You can see the full picture on the investor portal page.

Frequently Asked Questions

What is an investor portal?

An investor portal is a secure platform where a fund manager's investors log in to track their investments — viewing performance, capital account details, documents and tax forms, and reports, and in modern portals, managing bank accounts, funding capital calls, and receiving distributions. For the GP, it replaces ad hoc email-and-spreadsheet investor relations with a single system where each investor sees exactly what they're entitled to.

What's the difference between a private equity and a real estate investor portal?

Both handle capital commitments, calls, and distributions. A real estate investor portal adds a property dimension — investors expect asset-level context such as location, type, and status behind each investment, and the portal must handle deal-by-deal syndications as naturally as funds. A private equity portal centers on the fund lifecycle and cap-table relationships across multiple fund vehicles. Many managers run both structures, so a portal that handles funds and direct deals in one investor experience is ideal.

How secure is an investor portal?

Security comes down to permission enforcement: a well-built portal shows each investor only the holdings, documents, and reports tied to their own positions, with view and download permissions controlled separately and access scoped at every level. Look for a portal that enforces these controls consistently across documents, reports, and banking — and that routes sensitive actions like bank account changes through GP review rather than applying them silently.

How much does an investor portal cost?

Pricing varies widely with capability. A basic document-sharing portal is inexpensive but pushes the cost elsewhere — onto the manual work of keeping it current. A portal built on a platform that already manages your investors, distributions, and banking costs more upfront but eliminates the recurring cost of syncing data and handling money movement separately. The right way to compare is total cost of operating the portal each quarter, not the sticker price of the software.

Can investors get paid through the portal?

In a modern portal, yes. Investors can link a bank account, set a default, fund capital calls by ACH debit, and receive distributions — all inside the portal, with the GP approving banking changes. This is the clearest dividing line between a true investor portal and a branded document folder: whether money actually moves through it, or it only displays a PDF after the fact.