Bonus Depreciation in 2026: What Permanent 100% Expensing Means for Real Estate Syndications | Covercy

Capital Raising·10 min read

Bonus Depreciation in 2026: What Permanent 100% Expensing Means for Real Estate Syndications

The 2025 tax law made 100% bonus depreciation permanent, reversing the phase-out that had cut it to 40%. Here's how it works in a real estate deal, what it does to your investors' K-1s, the recapture catch, and how sponsors can use the tax story to raise capital without overpromising.

Kristen Erickson··10 min read

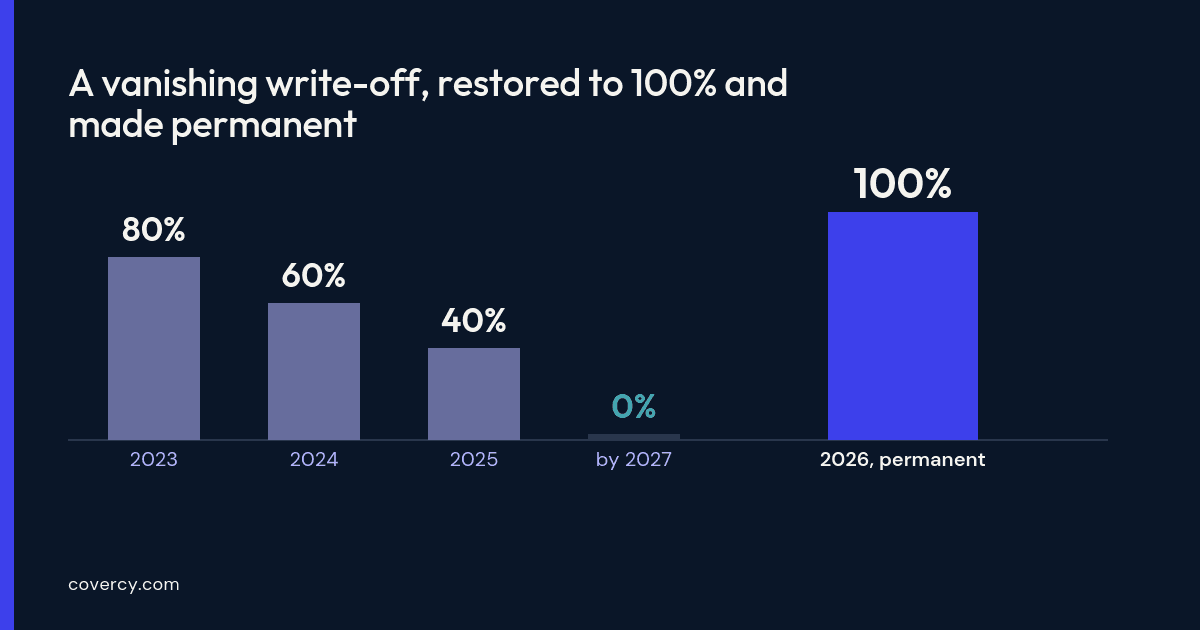

A year ago, bonus depreciation was on its way out. The 100% first-year write-off created in 2017 had been phasing down 20 points a year — 80% in 2023, 60% in 2024, 40% in 2025 — and was headed to zero by 2027. Every real estate sponsor running the numbers on a deal had to factor in a shrinking benefit. The 2025 federal tax law reversed that. The One Big Beautiful Bill Act, signed July 4, 2025, restored 100% bonus depreciation for qualifying assets acquired after January 19, 2025, and — for the first time — made it permanent. What was a closing window is now a durable planning input for every acquisition going forward.

For general partners (GPs) — the sponsors and fund managers who structure real estate syndications and funds — that change ripples straight through to the limited partners (LPs), the investors whose K-1s carry the resulting deductions. This article covers how bonus depreciation actually works in a real estate deal, why it makes cost segregation more valuable than ever, what it means for your investors, the recapture catch that the upbeat version leaves out, and how to fold the tax story into a raise responsibly. It is educational only — not tax, legal, or investment advice. The mechanics are general; the specifics depend on the deal and the investor, and every figure below should be confirmed with a qualified tax professional.

Note

Covercy is an investment management platform, not a tax advisor or accounting firm. Nothing here is tax advice. Bonus depreciation, cost segregation, and recapture all turn on facts specific to a property and an investor — always work with a CPA and tax counsel.

What changed in 2025

The core change is simple to state and significant in effect: 100% bonus depreciation is back and permanent. The uncertainty that had crept into deal underwriting — modeling a benefit that was smaller every year and disappearing entirely soon — is gone.

100% bonus depreciation applies to qualifying assets acquired after January 19, 2025 — a full first-year write-off, not the 40% that would have applied under the old phase-down.

Related Articles

The benefit is now permanent, rather than scheduled to expire, so it becomes a stable input to underwriting instead of a use-it-or-lose-it deadline.

Qualifying assets are generally those with a tax recovery period of 20 years or less — which, in a real estate context, means the shorter-life components a cost segregation study identifies, not the building itself.

A separate new provision for certain qualified production property (think manufacturing and production facilities) allows 100% expensing of some nonresidential real property under specific conditions and construction timelines — a niche but potentially large benefit for industrial and manufacturing-adjacent GPs.

How bonus depreciation actually works in a real estate deal

A building on its own is not a fast write-off. Commercial real estate is depreciated over 39 years (27.5 for residential rental) on a straight-line basis — a slow, steady deduction. Bonus depreciation doesn't apply to that structural shell. It applies to the components inside and around it that have much shorter tax lives: things like fixtures, certain fit-out, appliances, and land improvements classified as 5-, 7-, or 15-year property. The mechanism that separates those components out is cost segregation.

In a typical syndication, here is the chain: the sponsor acquires a property, commissions a cost segregation study that reclassifies a meaningful share of the purchase price into short-life property, and applies 100% bonus depreciation to that portion in year one. The result is a large first-year depreciation deduction — often far exceeding the deal's actual cash flow — that produces a paper loss. Because the syndication is a pass-through entity, that loss flows through to the investors on their K-1s in proportion to their ownership. Many LPs can use those passive losses to offset passive income elsewhere in their portfolio, which is precisely why the tax profile of a deal is often part of the story a sponsor tells.

The cost segregation connection

Cost segregation and bonus depreciation are two halves of one strategy, and the 2025 law makes the pairing stronger. A cost segregation study typically reclassifies somewhere in the range of 25–35% of a building's cost into 5-, 7-, and 15-year property. Under the old phase-down, only 40% of that reclassified amount could be written off immediately in 2025; the rest was depreciated over its normal life. With 100% bonus depreciation restored, the entire reclassified portion can be expensed in year one.

That mechanical change materially increases the first-year deduction a cost segregation study unlocks — which is why the studies are worth revisiting on deals underwritten during the phase-down years, and why they factor more heavily into acquisition math now. Whether a study makes sense on a given property is a cost-benefit question for the sponsor and their CPA, but the upside side of that equation just got bigger.

What it means for your investors' K-1s

For the LP, the visible result of all this shows up in one place: the Schedule K-1. A deal that generated a large first-year paper loss will report that loss on each investor's K-1, and the investor's tax advisor decides how it can be used given their situation and the passive-activity rules. This is genuinely valuable to investors — but it also raises the stakes on getting the K-1 right and getting it out on time.

K-1 delivery is a perennial pain point in this industry: investors chase sponsors for documents, K-1s arrive late and complicate personal filings, and a single deal with fifty LPs becomes fifty support conversations every spring. When the tax benefit is part of why investors committed in the first place, a sloppy or late K-1 undercuts the whole pitch. Delivering K-1s and other tax documents through the same investor portal where LPs already track their holdings — accurately, on schedule, every year — turns the annual tax-season scramble into a routine and reinforces the professionalism that keeps investors coming back for the next raise.

The catch: depreciation recapture

Here is the part the enthusiastic version of this story tends to skip. Bonus depreciation is an acceleration, not a free deduction — it front-loads deductions you would otherwise take over many years. When the property is sold, some of that benefit comes back in the form of depreciation recapture.

The short-life personal property that cost segregation carves out is generally subject to recapture at ordinary income tax rates, up to the amount of depreciation taken — which can be a higher rate than the capital-gains rate that applies to the rest of the gain. The building's own straight-line depreciation is subject to a separate rule (often taxed up to a 25% federal rate as unrecaptured gain). There is also timing to consider: the passive-activity-loss rules limit how much of a paper loss an investor can actually use in a given year, so the benefit may not be as immediate for every LP as a headline first-year number suggests. None of this makes bonus depreciation a bad deal — deferring tax and redeploying the cash has real value, and strategies like a 1031 exchange can affect the recapture picture. But an honest sponsor accounts for recapture in the story, rather than presenting the first-year deduction as pure upside.

Using the tax story to raise capital — responsibly

Tax efficiency is a legitimate and compelling part of a real estate offering, and sophisticated investors expect sponsors to understand it. The line to walk is between communicating the tax profile clearly and overpromising a specific outcome. Tax results depend on each investor's own situation — their income, their passive activity, their state — which means no sponsor can promise what a deduction will be worth to a given LP. The responsible approach is to describe the strategy and its mechanics, present illustrative rather than guaranteed figures, point investors to their own tax advisors, and keep marketing claims consistent with securities-law obligations around how private offerings are promoted.

Operationally, the tax story also has to be deliverable. If bonus depreciation is part of why an investor commits, the sponsor's job is to actually produce the accurate K-1 that carries the deduction — which brings the raise and the back office together. A fundraising flow that gets investors from interested to funded quickly, backed by reporting and K-1 delivery that hold up year after year, is what lets a sponsor make the tax case with confidence and then keep the promise. The pitch and the paperwork are the same commitment.

Before you rely on it: questions for your tax advisor

Bonus depreciation, cost segregation, and recapture interact in ways that depend entirely on the specific property, deal structure, and investor. Treat this article as a map of the terrain, not a route. Before underwriting a deal around the benefit or marketing it to investors, work through questions like these with a qualified CPA and counsel:

For sponsors: Does a cost segregation study pencil out on this property, and how much of the basis is likely to qualify for bonus depreciation? How should recapture be modeled into projected investor returns?

For investors: Given my income and passive activity, how much of the projected paper loss can I actually use this year — and what is my recapture exposure on exit?

For both: How do state tax rules treat bonus depreciation, and how does a planned hold period or a potential 1031 exchange change the analysis?

Is bonus depreciation still available in 2026?

Yes. The One Big Beautiful Bill Act, signed July 4, 2025, restored 100% bonus depreciation for qualifying assets acquired after January 19, 2025, and made it permanent — reversing the phase-down that had reduced it to 40% in 2025 and was set to eliminate it by 2027. See the IRS additional first-year depreciation FAQ for the official overview.

How does bonus depreciation work with cost segregation in real estate?

A cost segregation study reclassifies a portion of a building's cost — often roughly 25–35% — into shorter-life property (5-, 7-, and 15-year assets). That reclassified portion is eligible for 100% bonus depreciation, producing a large first-year deduction. The building's structural shell still depreciates over 27.5 or 39 years.

How does bonus depreciation affect an investor's K-1?

In a syndication, the first-year depreciation deduction creates a paper loss that passes through to investors on their Schedule K-1s in proportion to ownership. Many limited partners can use those passive losses to offset passive income, subject to the passive-activity-loss rules and their own tax situation.

What is depreciation recapture?

Depreciation recapture is the tax owed on previously claimed depreciation when a property is sold. The short-life property from a cost segregation study is generally recaptured at ordinary income rates up to the depreciation taken, while the building's straight-line depreciation is subject to a separate rule (often up to a 25% federal rate). Bonus depreciation accelerates deductions but does not eliminate recapture.

Bonus depreciation went from a benefit on borrowed time to a permanent fixture of the tax code — a real advantage for sponsors who understand it and communicate it honestly, recapture and all. The sponsors who turn it into durable investor trust will be the ones who can also deliver on the operational promise behind it: accurate reporting and on-time K-1s, year after year.