For real estate developers and fund managers raising capital, EB-5 occupies an unusual position in the capital stack. It is subordinated, patient, and available from a pool of investors — foreign nationals seeking US permanent residency — who are not accessible through the typical accredited investor channels. When structured correctly, EB-5 capital can fill mezzanine positions at costs well below conventional mez debt. The tradeoff is operational complexity: foreign investors, multi-currency flows, multi-year holds, and a regulatory framework that touches both securities law and US immigration.

This article focuses on the GP and developer perspective — specifically, what sponsors who want to raise and administer EB-5 capital need to understand about the program's mechanics, the operational responsibilities it creates, and how to manage those responsibilities at scale. It does not address EB-5 from the immigrant investor perspective and is educational in nature only. GPs considering EB-5 capital should work with qualified immigration counsel, securities attorneys, and EB-5 professionals — the program is complex and the consequences of missteps on either the securities or immigration side are significant.

EB-5 in Brief: What Developers Need to Know

The EB-5 Immigrant Investor Program, administered by USCIS, allows foreign nationals to obtain US permanent residency by investing in US commercial enterprises that create qualifying jobs. The EB-5 Reform and Integrity Act of 2022 (part of the Consolidated Appropriations Act) updated the program's investment thresholds: the minimum investment is $1,050,000, reduced to $800,000 for projects in a Targeted Employment Area (TEA) — a rural area or area with high unemployment as designated by the state and USCIS.

Each EB-5 investor's capital must be "at risk" throughout the investment period. That means the GP cannot guarantee return of capital or promise a specific yield — the investment must be genuinely subordinated to project risk. In exchange for bearing that risk, the investor receives a path to permanent residency rather than a purely financial return (though financial returns are common and permissible). The project must also create or preserve at least 10 qualifying full-time jobs per investor, either directly or indirectly through an approved regional center.

The holds are long. After investing, the EB-5 investor files an I-526 petition (or I-526E through a regional center), which USCIS must approve before the investor receives conditional permanent residency. The investor then holds the conditional green card for two years, after which they file an I-829 petition to remove conditions — a filing that requires demonstrating the job creation and investment requirements were met. Until the I-829 is approved, the investor's capital typically cannot be returned without jeopardizing the immigration outcome. In practice, this means EB-5 capital is often locked in a project for five years or more.

Most EB-5 projects are structured through a USCIS-designated Regional Center, which allows job creation to be counted indirectly using economic impact modeling rather than direct employment. Regional Center designation requires USCIS approval and ongoing compliance. Direct EB-5 investment — where a single business must directly hire 10 employees per investor — is less common in real estate development because of the headcount constraints.

Why Developers Use EB-5 Capital

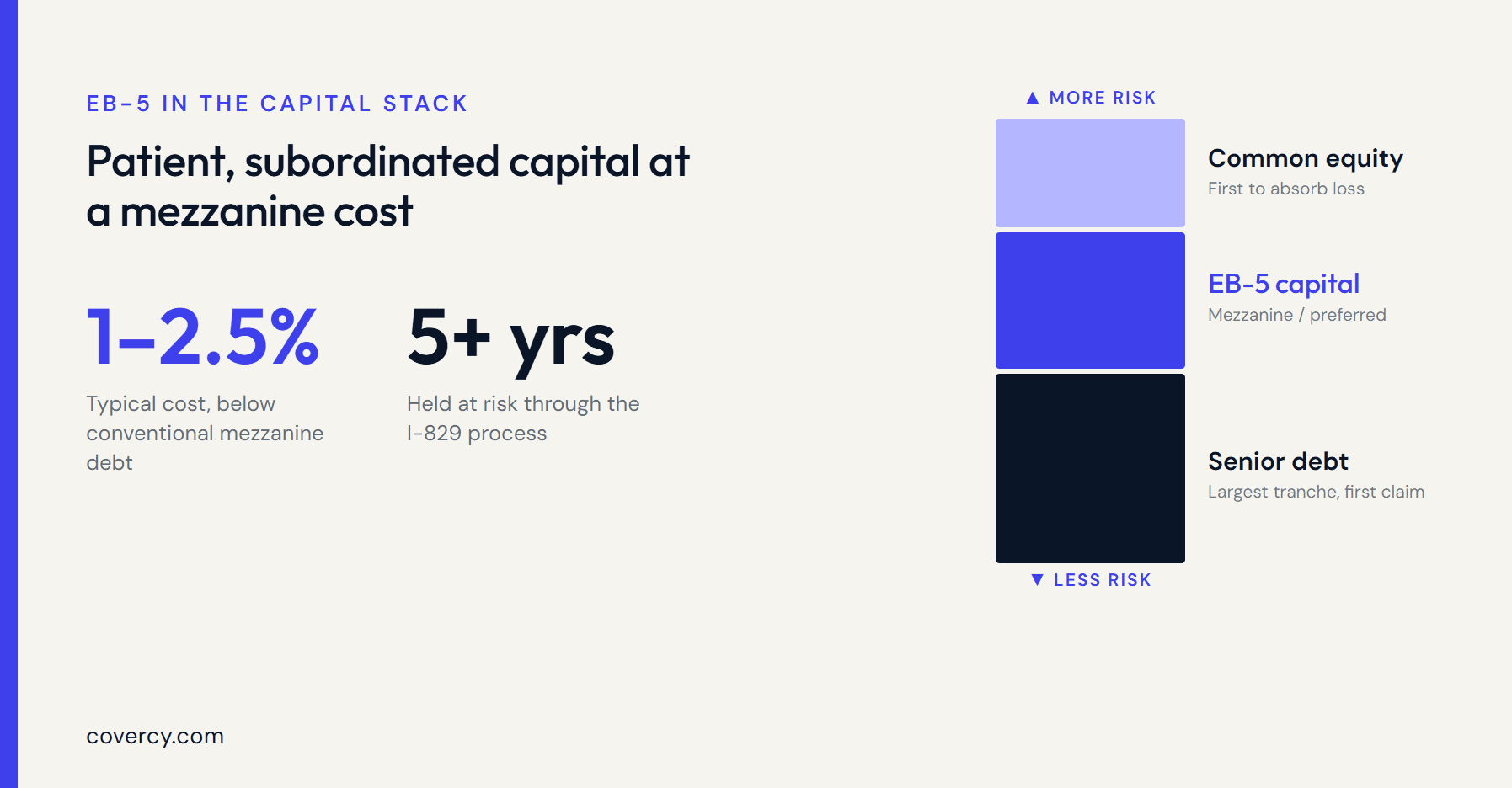

From a developer's perspective, the appeal of EB-5 capital is structural. It typically sits in the mezzanine or preferred equity position of the capital stack — senior to common equity but subordinate to senior debt. Because EB-5 investors are primarily motivated by immigration outcomes rather than maximizing financial return, they tend to accept below-market interest rates (often in the 1–2.5% range), making EB-5 one of the lower-cost forms of mezzanine capital available to real estate developers when sized correctly.

The patient nature of EB-5 capital is also operationally valuable for developments with long timelines — hotels, large mixed-use projects, workforce housing developments, and similar. Conventional mezzanine lenders want their money back on a defined schedule. EB-5 investors, by contrast, need their capital deployed and at risk throughout the I-829 process. A developer who can align project timelines with EB-5 hold requirements can use that capital without the refinancing pressure that shorter-duration mez creates.

The tradeoff is compliance burden. Every EB-5 investor is a foreign national whose immigration outcome is tied to your project's performance. USCIS filings, job creation documentation, offering document requirements under Reg D, ongoing investor reporting, and eventual capital return at I-829 approval all require discipline that a standard domestic raise does not. GPs who treat EB-5 as just another equity source without building the operational infrastructure to manage it properly create risk for themselves and their investors.

What GPs Must Operationally Manage for Foreign LPs

Managing EB-5 LPs is different from managing domestic accredited investors in four areas: onboarding, capital tracking, distributions and reporting, and compliance documentation. Each requires specific infrastructure.

Foreign investor onboarding requires collecting entity and tax identification information that differs from domestic standards. EB-5 investors invest through various entity types depending on their home country — individual accounts, foreign corporations, foreign limited partnerships — and many foreign nationals have tax identification structures (or lack US taxpayer identification entirely until their green card is issued) that don't fit a standard US onboarding form. You need a system that can capture country-coded contact information, record multiple entity types and their relationships to the investor, and track tax identification status across a multi-year hold.

Cross-border capital movement is the second area of operational complexity. EB-5 subscriptions often arrive via international wire, in the investor's home currency, and must be documented carefully for both SEC and USCIS compliance. Distributions — if the project generates preferred returns or periodic cash flow during the hold — also flow internationally. The operational challenge is tracking each investor's capital account accurately across currencies, recording every transaction with an auditable timestamp, and confirming that each payment cleared to the right account. Escrow arrangements are common in EB-5 raises, adding another layer to the capital tracking requirement.

Multi-year capital tracking is distinct from a typical value-add hold. In a standard CRE syndication, you distribute proceeds at sale or refinance and close the investor's account. In EB-5, the capital account stays open until the I-829 is approved — which may be years after the project's commercial completion. GPs need the ability to query each investor's capital balance as of any date during the hold, confirm compliance with the "at risk" requirement at the time of I-829 filing, and ultimately document the return of principal in a way that satisfies USCIS.

Investor reporting for EB-5 LPs is more demanding than for a domestic investor base. USCIS requires GPs to file annual reports (I-924A for Regional Center participants) documenting job creation and capital deployment. Beyond the regulatory filings, EB-5 investors — and their immigration attorneys — expect detailed periodic reporting on project status, capital deployment milestones, and job creation progress. Many investors are communicating through translators or in their home language, which adds a communication layer that typical quarterly reports don't address.

Compliance documentation — subscription agreements, operating agreements, USCIS filing confirmations, project status reports — must be organized and shareable on a controlled basis. The GP needs to be able to provide specific documents to specific investors (or their counsel) without exposing the full document library to all parties. Granular document access controls are not a nice-to-have in EB-5; they are operationally necessary.

How Covercy One Helps GPs Manage EB-5 Capital

The operational demands of EB-5 are exactly the kind of work that disconnected spreadsheets and email threads cannot scale. Covercy One's investment management platform is built for the infrastructure that EB-5 GPs need across foreign investor onboarding, cross-border banking, capital account tracking, investor reporting, and document management.

For foreign investor onboarding, Covercy One's contact management system supports country-coded contact records, multiple entity types, and the relationship mappings between individual investors and their investing entities. Each contact can capture entity type, tax identification, and country of origin — the data that EB-5 onboarding requires and that a standard domestic CRM was not designed to hold. Bulk CSV import supports bringing an EB-5 investor list into the platform without manual entry, with automatic column mapping and a review step to catch errors before they propagate.

Cross-border banking is supported through Covercy One's integrated banking capabilities, including the ability to manage bank accounts for multiple legal entities and record ACH and wire transactions with appropriate tagging. For EB-5 GPs who receive international wires into a US project account, the platform's banking table gives GPs a single view of all accounts — including investor-owned accounts — with per-holding assignment so each investor's capital flows to the right account.

Multi-currency handling is built into the platform's core financial layer. Monetary values display the currency of the relevant holding or account — not a hardcoded USD default — and CSV exports, distribution notices, and capital account data all reflect the holding's actual currency. For EB-5 raises that involve non-USD capital flows, this prevents the currency-mismatch errors that can complicate both investor reporting and USCIS documentation.

Capital account tracking in Covercy One's distribution management system maintains an immutable ledger of every transaction affecting each investor's position, with the ability to query balances as of any historical date. For EB-5 GPs who need to document capital deployment and balance at the time of I-829 filing — often years after the initial investment — as-of-date queries provide exactly that audit trail without manual reconstruction.

Investor reporting is handled in Covercy One's Report Studio, which lets GPs create branded periodic reports for specific holdings or share classes, export them as PDFs, and publish them directly to the investor portal. For EB-5 investors who receive quarterly or annual reports on project status, job creation milestones, and capital deployment, the reporting workflow handles the production and distribution of those reports through a single interface. Reports published to the portal are immediately accessible to the investors they're scoped to, without requiring manual email distribution.

Document management in Covercy One supports granular sharing controls: each document can be shared with a specific holding, share class, entity, or individual investor. Download permissions are enforceable per share, so the GP can distribute a document for viewing without enabling download. For EB-5 compliance documentation — subscription agreements, USCIS filing confirmations, project status certifications — the ability to share the right document with the right investor, with an audit trail of who accessed what, is the foundation of defensible record-keeping. The document sharing workflow in the investor portal makes that documentation accessible to investors without requiring the GP to field individual requests.

EB-5 capital is not the right fit for every project or every GP. It adds compliance complexity, requires qualified immigration and securities counsel, and locks capital in for an extended hold. But for the right development — a large multifamily, mixed-use, or hospitality project with a long timeline and the right job-creation profile — EB-5 provides a capital source with structural advantages that conventional debt and equity cannot replicate. For GPs who decide to pursue it, the difference between a manageable raise and an operational burden often comes down to whether the back-end infrastructure was built to handle the specific demands of foreign investor capital. Consult your immigration and securities counsel to determine whether EB-5 fits your project and structure.

See how Covercy One handles multi-currency capital accounts, cross-border banking, foreign investor onboarding, and compliance document management in a single platform built for GPs.

Request a demo (opens in a new tab)