Ask most multifamily investors how they pick a market and you will hear the same two answers: job growth and cost of living. They are real drivers. The problem is timing. By the time either one shows up clearly in the data, prices have usually already moved and the best entry points are gone. Those metrics tell you where people already went, not where they are going next.

A few lesser-known demand signals tend to move ahead of the headlines, and they are creeping into the conversation for good reason. If you could answer "where are people actually moving?" with real confidence, a lot more of your deals would be sitting on very good returns right now. Here are three demand signals worth factoring into how you choose your next market, and the specific markets each one points to. Track them, and the best cities for multifamily investing in 2026 start to look different from the consensus list.

Why job growth and cost of living lag the market

Job growth and cost of living are lagging indicators dressed up as leading ones. Employers expand after demand is already there. Affordability rankings reflect prices that have already reset. Both are worth watching, but each confirms a migration that started months or years earlier. The signals below work differently: they capture the pressures pushing people to move and the places quietly absorbing them, before those shifts turn into a bidding war.

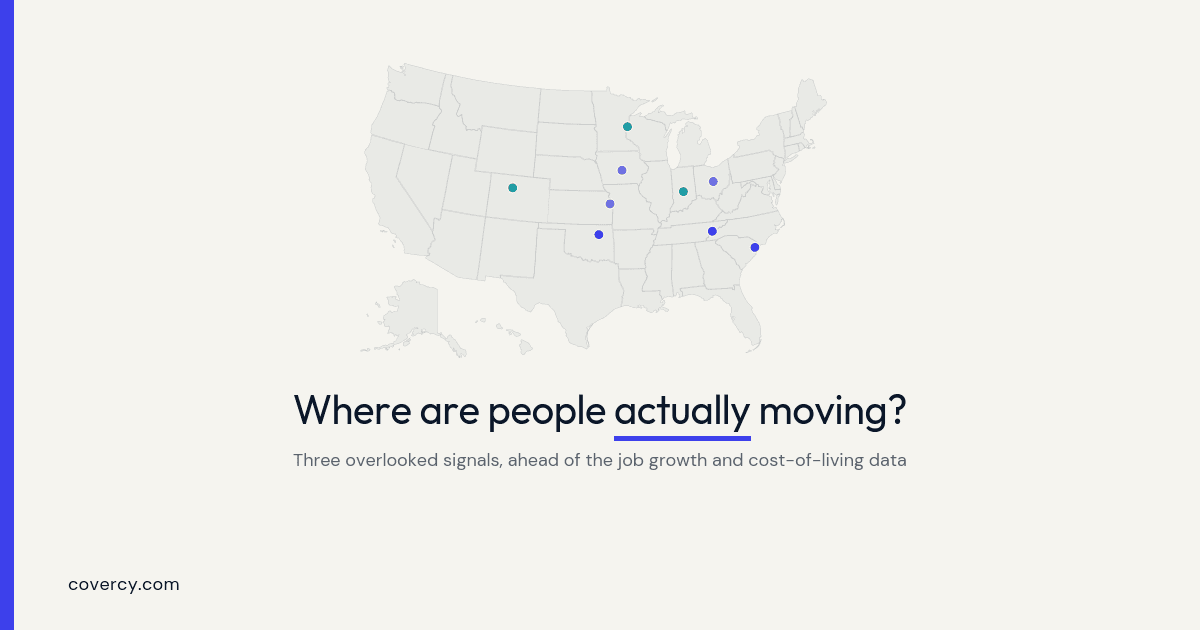

Signal 1: Insurance repricing is redrawing the map

Climate risk is showing up in insurance premiums long before it shows up in population data, and it is starting to move people. In 2024, a net 29,027 people left high-flood-risk areas of the U.S., the first such outflow since 2019, according to Redfin. Miami-Dade posted the worst outflow of any high-flood-risk county in the country. Looking ahead, insurer Kin found that 49% of homeowners weighing a move in 2026 cited climate risk as a specific reason, and Florida and California are now the two states homeowners most often name as places they would avoid.

For multifamily, that matters because rising premiums hit both sides of the ledger: they raise operating costs on assets you already own in exposed markets, and they push renters toward metros where insurance is not eating into the household budget. A lot of that displaced demand is landing in Minneapolis, Minnesota; Indianapolis, Indiana; and Denver, Colorado.